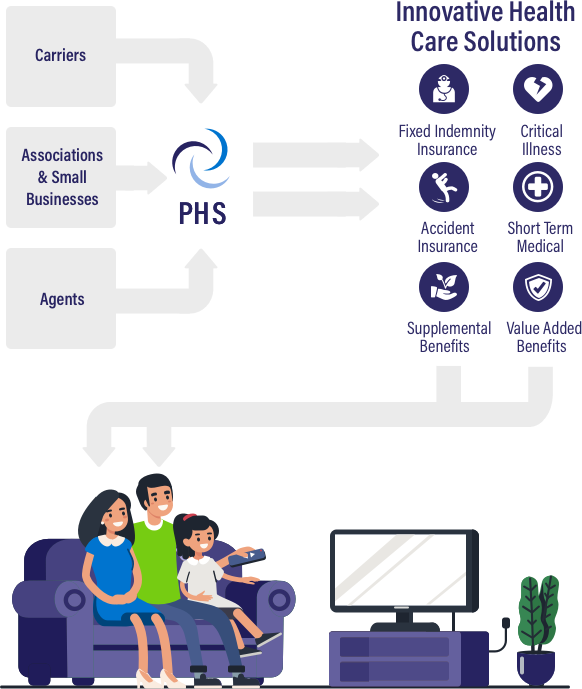

Agents

Associations & Small Businesses

Carriers

What We Do

Our Insured Products

Value-Added Benefits

Partner With Premier Health Solutions

We’re Here To Help Your Members

Learn More About Our Agency Services

Latest News from PHS

Premier Health Solutions Ranks #9 on Inc. Regionals List

Premier Health Solutions Ranks #366 on Inc. 5000

Supporting Neighbors During the Holiday Season

Our Business Insurance Management Services

Rich Benefit Packages At Competitive Rates

Your members deserve innovative and affordable business insurance options.

Your members deserve innovative and affordable business insurance options.

We know that many entrepreneurs or small business owners can't access traditional insurance. Other members struggle with high deductibles that their savings couldn't match. Others may have a family history of a serious health condition, while some are looking for coverage in-between seasonal jobs or after their spouse gets laid off.

No matter where your members start, we'll help you create a benefit portfolio that gets them to their future.

Premier Health Solutions is an exclusive administrator for The Health Depot Association and Affiliated Workers Association. This allows us to provide rich benefit packages at affordable rates for your members. We use a mix of insured and non-insured products, and then monitor how your members use them over time.

For example, members who are using their critical illness insurance benefits may find even more cost-savings from prescription coverage or discount prescription plans. These could help manage the costs of a long-term illness. Or, your short-term health insurance members may love the flexibility of telemedicine appointments and direct-to-consumer lab services during their time of transition.

By building out a benefit-rich portfolio, coupled with always-on member services, your members get a concierge approach. Our plans are truly made for today's families: flexible, affordable, and made to meet their unique needs.

We're ready to make your healthcare management easier. Are you?

PHS Privacy Policy - https://mu.staging.premierhsllc.com/phs-privacy-policy/